Replacement Cost

Most individuals, were their home to be completely destroyed, would want their home rebuilt exactly how it was or at least functionally similar. Insurance can be purchased for this kind of loss settlement; it is known as a Replacement Cost Homeowners Policy.

A Replacement Cost Homeowners policy will pay the cost to repair or rebuild your home up to the amount you have the home insured for. In fact, even if you decide you do NOT want to have your home rebuilt and you would like to relocate; the policy will pay the fair market value of the home at the time of the loss.

So, how do you know you have your home properly insured? It all starts with a “Replacement Cost Estimate”. This is where your agent gathers lots of information about the physical characteristics of your home such as number of stories, square feet and so on. All of this information is then entered into software that then calculates the Replacement Cost of you home.

The Replacement Cost of your home is likely more than your market value since market value takes into account the value of your land, taxes, school districts and other things that will have no bearing on the actual reconstruction cost of the home. The Replacement Cost of your home is also likely much higher than the cost of a newly built home for the following reasons:

- Often times, when a NEW home is built, it isn’t the only one being built at that time by the contractor so they can get better deals on materials, especially if it was part of a new subdivision development where many homes were being constructed at once

- When a home is destroyed, there is a lot of debris that will have to removed and excavated, driving up the cost

- Special permits have to be obtained for a tear down and rebuild, these can be costly

- Specialized equipment may be needed as well

Marshall, Swift and Boeckh (MSB) is an industry leading company that not only works with the insurance industry but also the construction and real estate industry as well. They provide new and reconstruction estimates as well as appraisal service for those industries.

Co-Insurance Penalties

What is that you ask? If you have home insurance, this is part of your policy…read on.

MSB estimates that 61% of homes in the US are underinsured for replacement cost by as much as 18%!

What do I mean by underinsured? In the context of what we are discussing here, it would mean you would not have enough coverage to fully rebuild your home and could be left paying thousands out of pocket! That’s pretty scary, especially considering MSB’s estimates noted above!

To compound this problem, most home insurance policies will allow a home to be insured for as little as 80% of the total replacement cost. This means if you have a home with a reconstruction cost of $200,000, they would only require you to insure the home to $160,000 to qualify for their replacement cost policy. This can be a dangerous practice since if you end up being below that 80% requirement you may end up having to pay what is called a co-insurance penalty. This is essentially a penalty for not insuring to the full value of the home. Why would the company care if you fully insured a home or just for a portion of it? I mean, you are paying them a premium for it right?

Consider this scenario:

I buy a home in an area with depressed market values. I pick up a steal of a deal on a home and pay $50,000 for the house. It’s an older home; built in the early 1900’s and is about 2500 square feet. My agent tells me the replacement cost on this is going to end up being $750,000 due to the unique construction quality that was common in the early 1900’s (They sure don’t make em’ like they use to!)

Shocked at the replacement cost I ask to insure the home for a substantial amount less, say $100,000, but I want partial losses to still be repaired for the full cost of the repairs. Now, most companies will have safeguards in place to prevent this, but let’s just say for arguments sake, I get the agent to go ahead and insure this at replacement cost of $100,000.

Insurance policy premiums, when they are established are done under the assumption that the VAST majority of losses that will occur will be minor or smaller losses and will only have to payout a small portion of the amount of insurance purchased.

Think about it for a second…if you are the insurance company and somebody wanted to insure something with you that cost $10,000 and it was guaranteed that the item would be destroyed in the first year and need to be replaced, how much would the insurance be? $10,000, that’s how much, maybe they’d even charge a bit more than that for administrative charges etc. It’s a guaranteed loss! Of course they aren’t going put themselves in a position to lose money on the deal!

So this how the pricing goes…it assumes or hedges its bets you won’t have total losses, that is why your premiums are always a fraction of the total value of the thing that you are insuring.

Now, back to my scenario, if my home has a replacement cost of $750,000, and I only insured it for $100,000, isn’t it very likely that a partial loss, where the home isn’t completely destroyed could easily make it to the $100,000 mark or close to it? Yes! Now the company would not have been collecting adequate premium for that home.

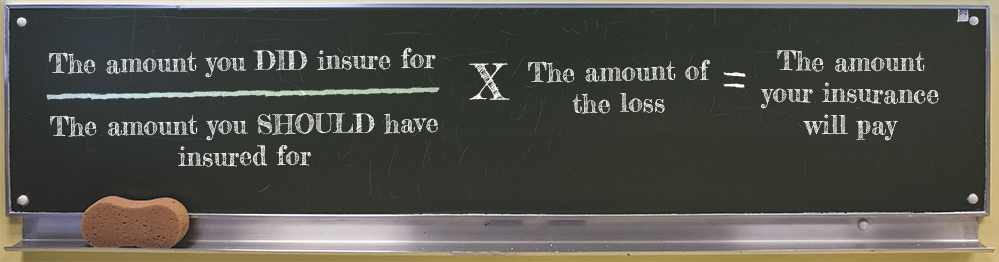

That is why they care how much you are insured for, to ensure they are collecting adequate premium. And this is also why companies have co-insurance penalties; it makes you put some skin in the game. If you underinsure your house too much, you could end up paying significant sums out of pocket at the time of loss beyond what your deductible is. How much you would have to pay if you are underinsured is based on a formula known as (Did/Should X Loss):

This can leave you paying thousands out of pocket depending on how much you are under insured for!

That’s pretty scary stuff; especially considering MSB’s estimates of 61% of homes being underinsured by 18%. That’s toeing an awfully close line to the co-insurance penalty….not a position I would want to be in!

Unfortunately, since many home policies will allow homes to be insured to as little as 80%, there are many agents out there that will do just that, using it as a form of “competitive edge”. The only thing “competitive” about this strategy is that you are possibly paying less for certainly less insurance coverage. It’s a dangerous game to play, a game we don’t play. Our goal is to do our best to help you insure your home for what it could cost you in the event of the loss, and to avoid exposing you to tricky traps like coinsurance penalties.

Have question about how much your home is insured for? Call us!

Darin Mohrman

I’m a former aspiring “ski-bum” turned insurance professional.I was licensed in 2002 and in 2013 I obtained my Certified Insurance Counselor (C.I.C.) designation. I'm married to an amazing woman, have a wonderful son and a cat.I enjoy travelling, music, craft beer, woodworking, collecting and restoring antique tools and all things computer and tech related.

Latest posts by Darin Mohrman (see all)

- Skip the “Snail Mail” - February 17, 2021

- Your Waterfront Home May Not Be Adequately Insured - February 12, 2021

- Citizens Insurance SafeTeen Program - February 9, 2021